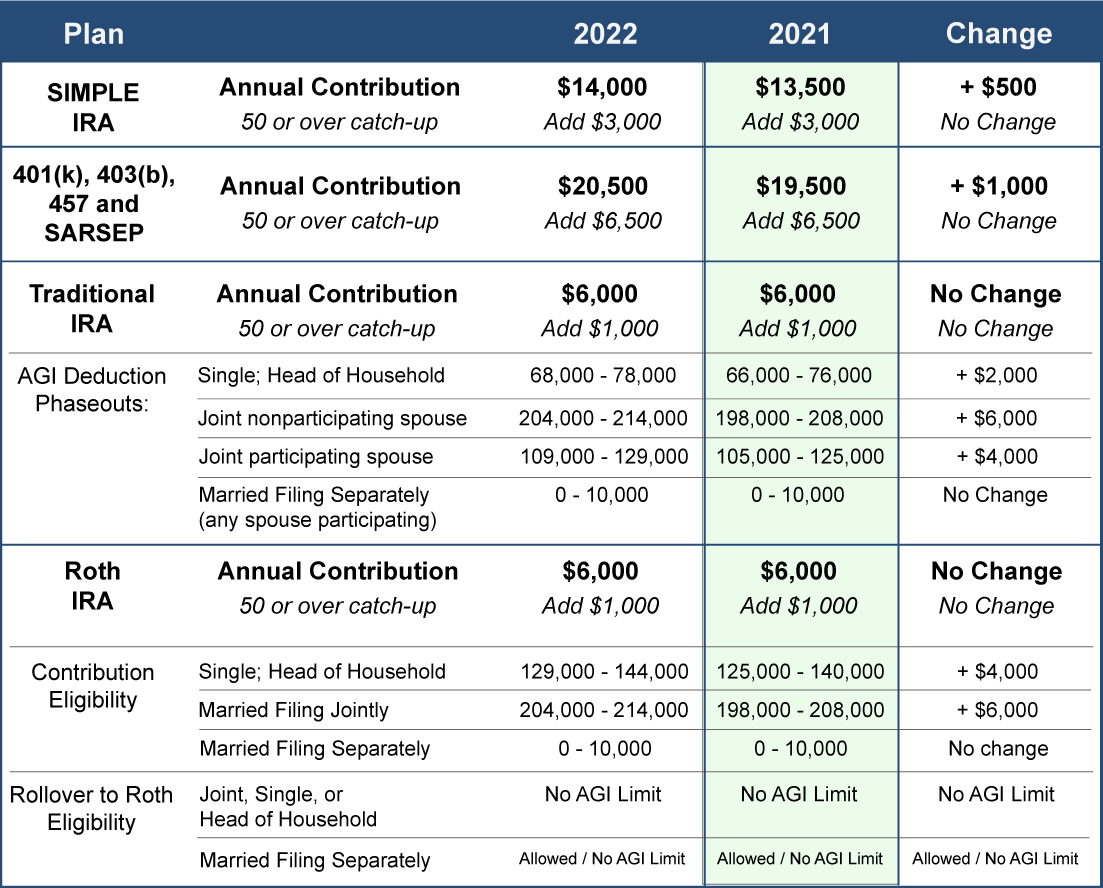

As part of your planning for next year, now is the time to review funding your retirement accounts In 2022. With the cost of living calculations and increases in inflation, higher phaseout limits make many more taxpayers eligible for fully deductible contributions. So plan now to take full advantage of this tax benefit. Below you will find a summary of annual contribution limits for the more popular programs. But REMEMBER, THERE ARE OVER 29 DIFFERENT TYPES OF PLANS. Your Tax Planner will discuss with you how you can maximize the tax benefits depending on your unique situation.

How to Use:

- Identify the type(s) of retirement savings plans that you currently use.

- Note the annual savings limits of the plan for next year and adjust your savings to take full advantage of the annual contributions. Remember, a missed year is a missed opportunity that does not come back.

- If you are 50 years or older, add the catch-up amount to your potential savings total.

- Take note of the income limits within each plan type.

- For traditional IRA’s, if your income is below the noted threshold, your taxable income is reduced by your contributions. The deductibility of your contributions is also limited if your spouse has access to a plan.

- In the case of Roth IRAs, the income limits restrict who can participate in the plan.

If you have not already done so, also consider:

- Setting up new accounts for a spouse or dependent(s)

- Using this time as a chance to review the status of your retirement plan including beneficiaries

- Reviewing contributions to other tax-advantaged plans like Flexible Spending Accounts (health care and dependent care) and prepaid medical savings plans like Health Savings Accounts. See below

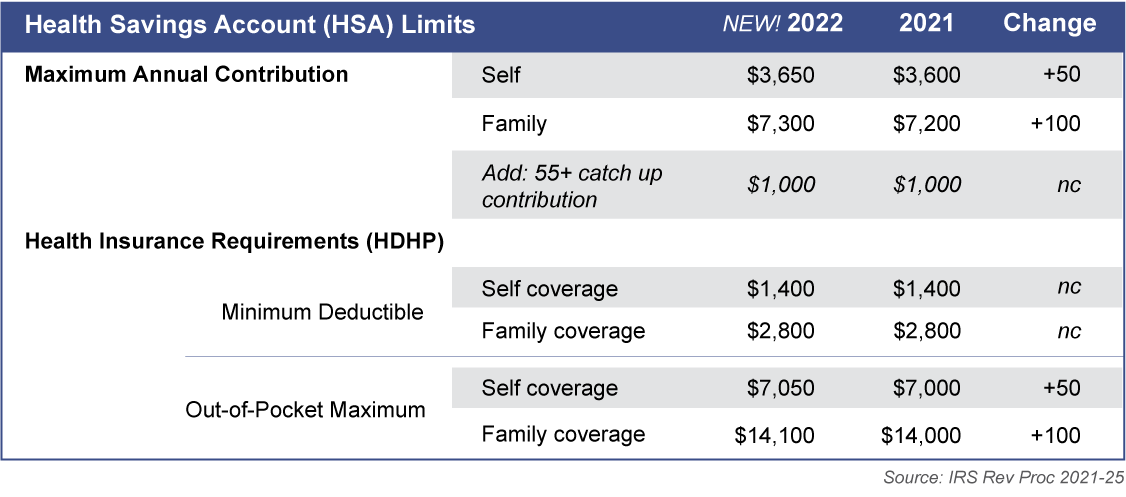

2022 Health Savings Account Limits

New contribution limits are on the horizon

The savings limits for the ever-popular health savings accounts (HSA) are set for 2022. The new limits are outlined here with current year amounts noted for comparison. So plan now for your contributions.

What is an HSA?

An HSA is a tax-advantaged savings account whose funds can be used to pay qualified health care costs for you, your spouse, and your dependents. The account is a great way to pay for qualified health care costs with pre-tax dollars. In fact, any investment gains on your funds are also tax-free as long as they are used to pay for qualified medical, dental, or vision expenses. Unused funds may be carried over from one year to the next. To qualify for this tax-advantaged account you must be enrolled in a high-deductible health plan (HDHP).

The Limits:

Note: An HDHP plan has minimum deductible requirements that are typically higher than traditional health insurance plans. To qualify for an HSA, your coverage must have out-of-pocket payment limits in line with the maximums noted above.

The key is to maximize funds to pay for your medical, dental, and vision care expenses with pre-tax money. By building your account now, you could have a nest egg for unforeseen future expenses.

WANT MORE?

Check out our podcasts and webinars on these topics:

Is Your Pension Plan Fully Funded? Plan Your 2021 Retirement Contributions

Follow Our Practical Tax Podcast for more content!